In the fast-moving world of algorithmic and futures trading, a backtest that looks perfect on paper often crumbles in live markets. That’s where trading strategy robustness testing comes in. It’s the critical process that separates overfitted curve-fits from strategies built to survive real-world volatility, regime shifts, and execution realities.

Table of Contents

- What Is Trading Strategy Robustness Testing?

- Why Trading Strategy Robustness Testing Matters More Than Ever in 2026

- Key Methods for Robustness Testing Trading Signals

- Step-by-Step Trading Strategy Robustness Testing Process

- Common Pitfalls to Avoid in Trading Strategy Robustness Testing

- Testing a Trading Signal vs. a Full Strategy

- Robustness Testing Methods at a Glance

- Robustness Checklist

- Deploying Robust Strategies Live: PickMyTrade Automation for US Futures Trading

- Conclusion: Make Trading Strategy Robustness Testing Your 2026 Competitive Edge

- Most Asked FAQs

Whether you trade stocks, forex, or US futures, mastering trading strategy robustness testing in 2026 is no longer optional—it’s your edge against drawdowns and emotional trading failures. This guide walks you through proven methods, step-by-step processes, and how to turn robust strategies into automated profits.

What Is Trading Strategy Robustness Testing?

Trading strategy robustness testing evaluates whether a trading system performs reliably across varied market conditions—not just the specific historical data it was optimized on. It measures resistance to overfitting, parameter changes, data noise, and unseen future scenarios.

A robust strategy maintains consistent metrics (win rate, Sharpe ratio, drawdown) even when you introduce small tweaks, shuffle trade order, or simulate slippage. In contrast, a fragile one collapses outside its narrow training window.

Why Trading Strategy Robustness Testing Matters More Than Ever in 2026

Markets in 2026 are shaped by AI-driven liquidity, rapid regime changes, and higher execution costs. Most retail traders still rely on single backtests and wonder why live results disappoint. Proper trading strategy robustness testing dramatically raises the probability that your edge survives:

- Avoiding overfitting (the #1 reason strategies fail live)

- Preparing for black-swan events and volatility spikes

- Confirming statistical significance over random luck

- Building trader confidence before risking capital

Recent analyses show strategies passing multi-path robustness checks outperform those that don’t by wide margins in forward performance.

Key Methods for Robustness Testing Trading Signals

Here are the battle-tested techniques every serious trader should use:

1. In-Sample / Out-of-Sample (IS/OOS) and Walk-Forward Analysis

Split data (e.g., 70/30) and re-optimize periodically in rolling windows. Walk-forward matrix testing simulates real forward deployment.

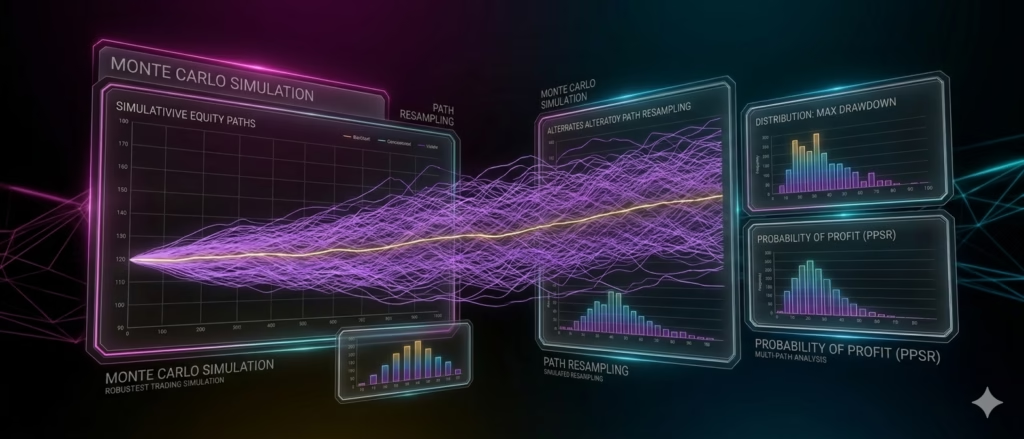

2. Monte Carlo Simulations

Reshuffle trades, resample with replacement, or permute price changes to create thousands of alternative paths. New 2026-era variants in tools like StrategyQuant include:

- MACHR Block Randomization (regime sequence stress)

- Parameter Jitter (missed trades + P/L variance)

- Randomly Degrade Execution (slippage modeling)

- SWAP Randomization (funding cost changes)

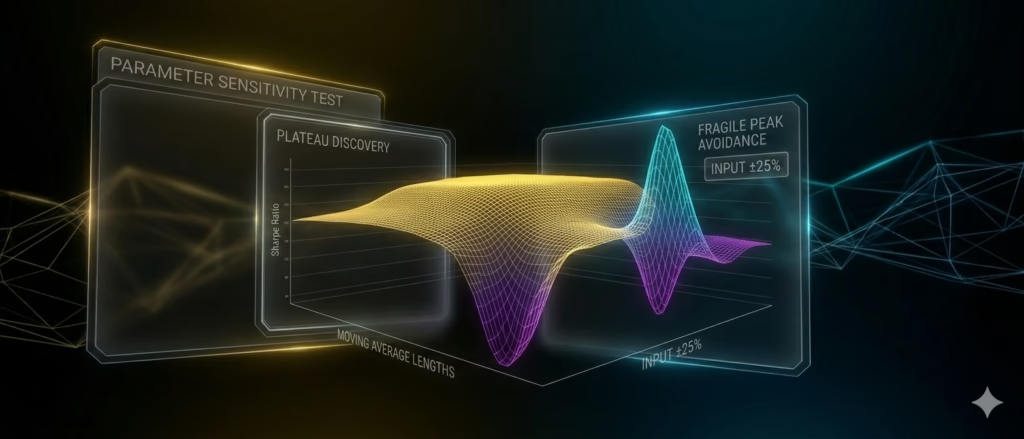

3. Parameter Sensitivity & Stability Testing

Vary inputs ±10–25% and plot performance surfaces. Stable “plateaus” indicate robustness; sharp peaks signal fragility.

4. Combinatorial Purged Cross Validation (CPCV)

Generate dozens of purged IS/OOS paths to calculate Probability of Backtest Overfitting (PBO <15% is strong) and Probability of Positive Sharpe Ratio (PPSR).

5. Noise, Liquidity & Stress Testing

Add random price noise, simulate delayed entries, or test across multiple markets/timeframes. Liquidity testing reveals slippage impact in fast US futures markets.

6. Vs. Random & Multi-Market Validation

Benchmark against purely random strategies and test the same rules on correlated instruments (e.g., ES futures → NQ or equities).

Click Here To Automate TradingView Strategy

Step-by-Step Trading Strategy Robustness Testing Process

- Build baseline — Develop and optimize on in-sample data with clear rules.

- Run core tests — IS/OOS + Walk-Forward + Monte Carlo (1,000+ runs).

- Apply sensitivity checks — Parameter jitter, noise addition, execution degradation.

- Measure metrics — Track PBO, PPSR, max drawdown distribution, Sharpe stability.

- Validate multi-universe — Test on additional markets and timeframes.

- Stress extremes — Synthetic shocks, higher slippage, regime blocks.

- Pass or iterate — Only deploy if metrics remain acceptable across 80%+ of simulations.

Common Pitfalls to Avoid in Trading Strategy Robustness Testing

- Single-path walk-forward (lucky splits hide weaknesses)

- Ignoring real costs (commissions, slippage, funding)

- Over-optimizing without stability checks

- Using short datasets lacking bull/bear regimes

- Testing only on one market

Testing a Trading Signal vs. a Full Strategy

A signal is the entry/exit trigger itself; a strategy wraps that signal with position sizing and risk rules. Robustness tests apply to both, but signal-level testing focuses specifically on hit-rate stability and decay — does the signal keep firing at a similar accuracy as conditions shift, independent of how much size or risk gets layered on top.

Robustness Testing Methods at a Glance

| Method | What it exposes | Pass guideline | Typical tool |

|---|---|---|---|

| Walk-forward analysis | Parameter overfitting over time | Walk-forward efficiency ≥ 50–60% | Build Alpha, StrategyQuant, Python |

| Monte Carlo (trade reshuffle) | Dependence on lucky trade order | 95th-percentile drawdown survivable | Python, StrategyQuant |

| Parameter sensitivity | One “lucky” parameter set | Profitable across ±20% parameter region | Any backtester |

| Out-of-sample / CPCV | Data mining bias | PBO < ~0.2 | Python (mlfinlab) |

| Noise / execution stress | Fragility to slippage & price jitter | Still profitable with 1–2 tick degradation | Build Alpha, custom sim |

These thresholds are practitioner rules of thumb, not universal standards — treat them as starting guidelines and calibrate to your own market and timeframe.

Robustness Checklist

- Split data into in-sample and out-of-sample before any optimization

- Run walk-forward analysis across multiple rolling windows

- Run Monte Carlo trade-reshuffle simulations, check 95th-percentile drawdown

- Test parameter sensitivity across a ±20% region around your chosen values

- Run CPCV or a purged cross-validation pass, check PBO

- Apply noise/slippage stress (1–2 tick degradation) and re-check profitability

- Compare against a random-entry benchmark on the same exits

- Validate across at least one additional, related market

- Confirm sample size — 100+ out-of-sample trades minimum

- Document every pass/fail threshold before you look at the results, not after

Deploying Robust Strategies Live: PickMyTrade Automation for US Futures Trading

Once your strategy passes trading strategy robustness testing, the next step is flawless execution. Enter PickMyTrade — a purpose-built no-code automation platform tailored for US futures markets.

PickMyTrade connects TradingView alerts directly to Tradovate (and other brokers like Rithmic, IB, TradeStation) for 24/7 automated execution of futures contracts such as ES, NQ, YM, and RTY. No coding required: simply copy webhook URLs into your alerts and let the cloud platform handle precision entry, risk management, and multi-account scaling.

Traders using PickMyTrade report eliminating missed signals, emotional interference, and latency issues—turning rigorously tested strategies into consistent, hands-off futures profits. With unlimited strategies, tickers, and 24/7 support, it’s the perfect bridge from robustness testing to live US market automation.

Conclusion: Make Trading Strategy Robustness Testing Your 2026 Competitive Edge

Stop gambling on untested backtests. Incorporate trading strategy robustness testing into every strategy development cycle and watch your live performance improve dramatically. Combine it with automation tools like PickMyTrade, and you’re positioned for scalable success in futures and beyond.

Start today: pick one of your existing strategies, run a full Monte Carlo + CPCV suite, and measure the difference.

Ready to build bulletproof strategies? Bookmark this guide and share it with fellow traders.

Most Asked FAQs

It’s the process of stress-testing a strategy across thousands of simulated market paths, parameter variations, and execution realities to confirm it’s not overfitted and likely to hold up in live trading.

They pass on one specific historical path but lack robustness to noise, slippage, regime changes, or parameter drift—issues trading strategy robustness testing uncovers early.

Backtesting shows historical performance on one path. Robustness testing runs hundreds or thousands of alternative paths and stress scenarios to prove reliability.

No single method wins. Combine Monte Carlo simulations, CPCV (for PBO), parameter sensitivity, and multi-market testing for comprehensive validation.

Absolutely. Platforms like PickMyTrade make it simple to automate proven strategies on ES, NQ, and other futures via TradingView webhooks with zero coding and 24/7 execution.

Robustness testing of trading signals checks whether a signal keeps working when conditions change — different data, parameters, markets, and execution assumptions. The five core tests are walk-forward analysis, Monte Carlo simulation, parameter sensitivity, out-of-sample validation, and noise/stress testing. A signal that only works on the exact data it was optimized on is overfit, not robust.

Practitioners commonly want 100+ trades minimum out-of-sample; fewer means Monte Carlo confidence intervals stay too wide to trust.

A backtest measures past performance once; robustness testing perturbs data, parameters, and execution to see whether that performance survives change.

Disclaimer:

This content is for informational purposes only and does not constitute financial, investment, or trading advice. Trading and investing in financial markets involve risk, and it is possible to lose some or all of your capital. Always perform your own research and consult with a licensed financial advisor before making any trading decisions. The mention of any proprietary trading firms, brokers, does not constitute an endorsement or partnership. Ensure you understand all terms, conditions, and compliance requirements of the firms and platforms you use.

Also Checkout: Debugging TradingView Strategies: 10 Pine Script Fixes

Connect your alerts with PickMyTrade — automated trade execution, no coding required. Start free →