Algo traders are losing money to hidden overfitting every day. Walk forward testing algos change that forever.

In 2026, with volatile US futures markets and AI-driven strategies exploding, walk forward testing algos have become the non-negotiable standard for building strategies that actually survive live trading. Forget one-time backtests that look perfect but blow up in real time. Walk forward testing algos simulate exactly how your strategy will perform as markets evolve—re-optimizing parameters on rolling windows and validating on truly unseen data.

If you trade automated futures (ES, NQ, CL, or any US contract), mastering walk forward testing algos is now your edge.

What Are Testing Algos and Why They Matter in 2026

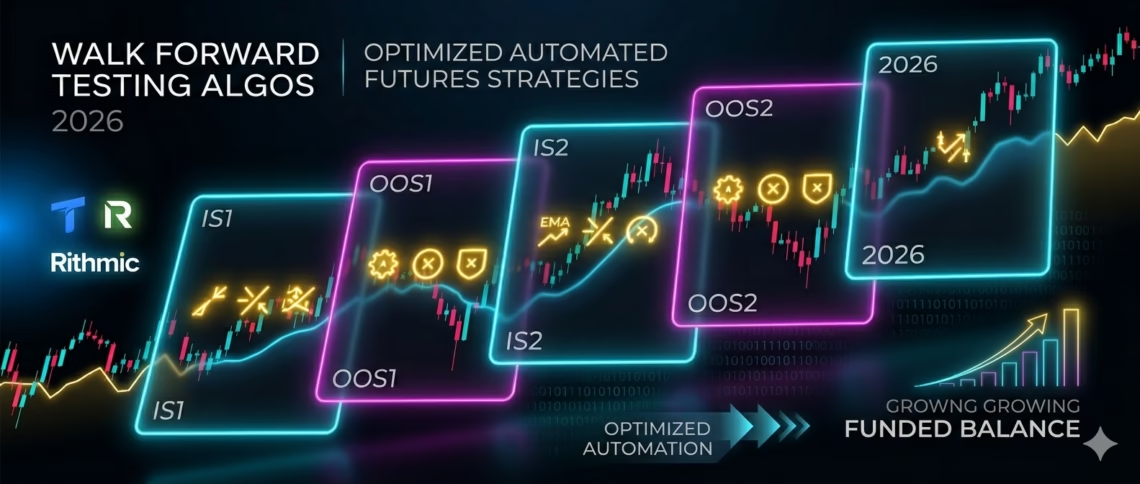

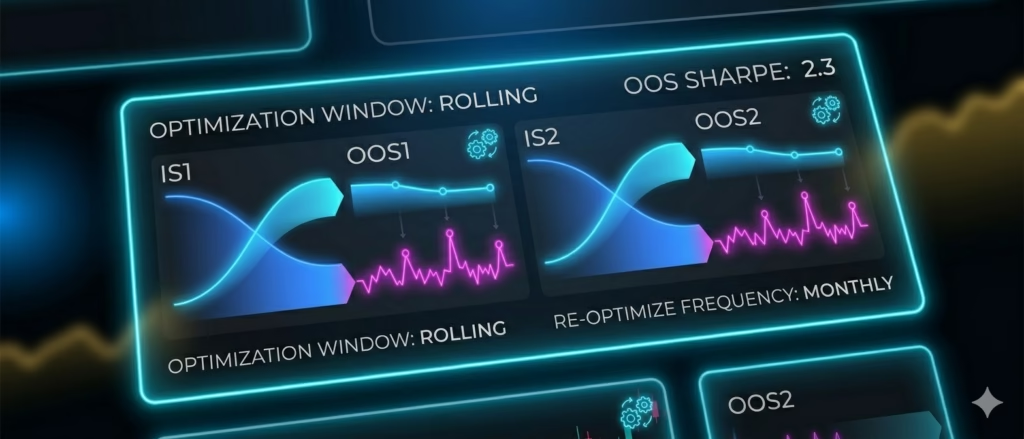

Testing algos divide your historical data into multiple rolling periods:

- In-sample (IS) window: Optimize parameters (e.g., EMA lengths, stop levels).

- Out-of-sample (OOS) window: Test those parameters on fresh data you’ve never seen.

Then shift the window forward, re-optimize, and repeat.

This rolling process—popularized in 2025–2026 by platforms like QuantConnect and detailed in recent quant research—mimics real trading far better than static backtests. Traditional optimization overfits to past noise. Testing algos prove your strategy adapts to changing regimes (bull, bear, chop).

Result? Robust, profitable algos that keep working when markets shift.

2025–2026 Updates: Why Walk Forward Testing Algos Are Now Essential

The game changed fast:

- March 2025: Interactive Brokers / PyQuant News declared walk-forward analysis “the future of backtesting,” highlighting its superiority for dynamic markets.

- 2026 Medium case studies: Traders published full WFO + Monte Carlo validated strategies for ADA-USD and MSFT, proving consistent OOS performance through 2026 stress tests.

- QuantConnect & TradingView enhancements: Native WFO scheduling and custom Pine scripts (like Deeptest library) now make rolling optimization accessible without PhD-level coding.

- Futures focus: 2026 automated futures guides explicitly recommend walk forward testing algos alongside regime filters to handle high volatility and slippage in US markets.

Smaller prop firms and retail traders ignoring this are watching strategies die. Serious funded traders using walk forward testing algos are scaling faster and safer.

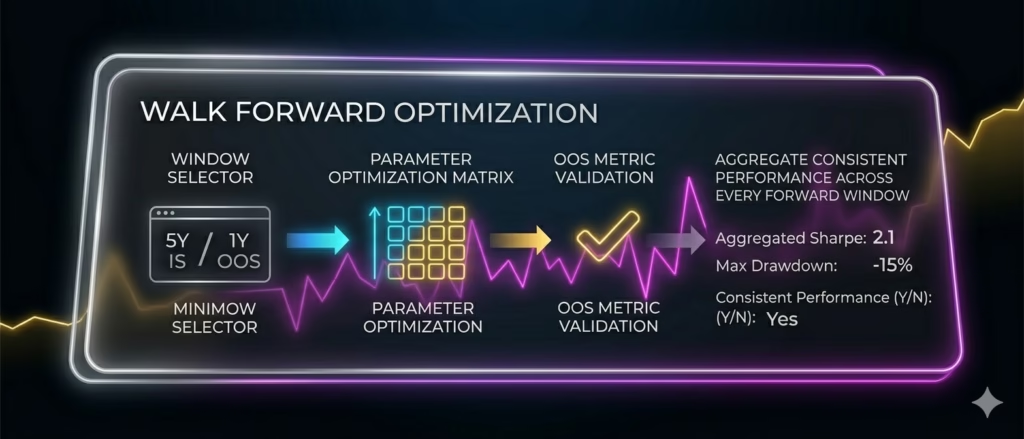

How Testing Algos Prevent Overfitting (Step-by-Step)

Here’s the proven process (used by pros on QuantConnect and Python setups):

- Choose windows: e.g., 5-year IS optimization + 1-year OOS testing (adjust for your timeframe).

- Optimize parameters on IS data (grid search or genetic algorithms).

- Apply best parameters to next OOS period and record metrics (Sharpe, drawdown, profit factor).

- Roll forward: Shift windows by the OOS length and repeat until present day.

- Aggregate all OOS results—only strategies with consistent performance across every forward window survive.

QuantInsti 2025 example: Portfolio allocation from 2010–2025 showed dramatic realism gains versus one-shot backtests.

Pro tip for futures: Run WFO on minute or daily data for NQ/ES to capture intraday regime shifts. Combine with Monte Carlo for tail-risk stress.

Click Here To Automate Futures Trading

Walk Forward Testing Algos for US Futures Traders: Automate the Edge

US futures demand speed and adaptability—perfect for walk forward testing algos.

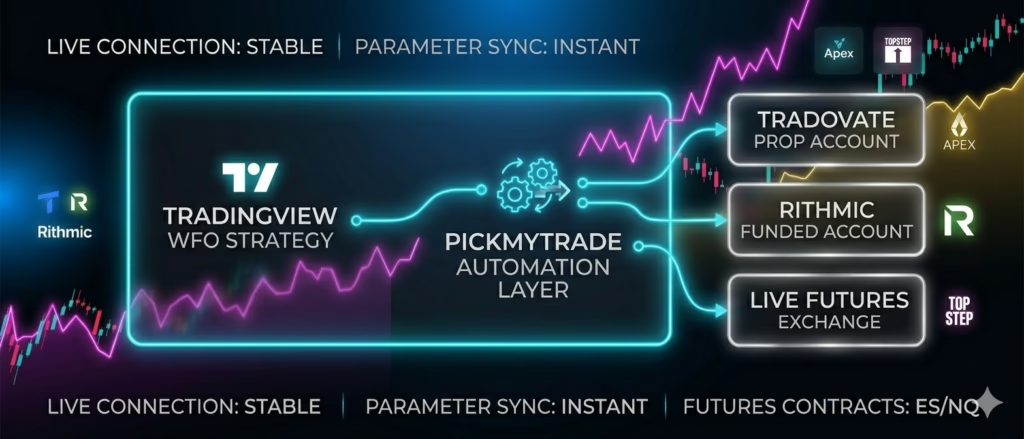

Build and validate your strategy in TradingView (using free WFO Pine scripts). Once optimized and proven robust across multiple forward periods, deploy instantly.

Enter PickMyTrade—the smartest automation layer for futures trading on US markets.

PickMyTrade connects your TradingView strategy directly to Tradovate or Rithmic-powered accounts. Run unlimited optimized strategies 24/7 across multiple funded/prop accounts with zero manual updates. When markets shift, simply re-run your WFO analysis, tweak parameters in TV, and PickMyTrade pushes the new logic live.

No coding. No downtime during re-optimization. Full support for Apex, TopStep, and every major US futures prop firm. One low monthly fee unlocks the exact automation serious traders need in 2026.

The Bottom Line: Make Testing Algos Your 2026 Superpower

Static backtests are dead. Testing algos deliver the only performance numbers you can actually trust.

Adopt them now—test rigorously, automate smartly with tools like PickMyTrade, and watch your funded futures accounts compound while others chase curve-fitted ghosts.

The 2026 markets reward adaptable traders. Walk forward testing algos are how you stay ahead.

Most Asked FAQs

Walk forward testing algos (WFO/WFA) roll optimization and validation windows forward through time. You optimize on recent in-sample data, test on the next unseen out-of-sample period, then repeat—creating a realistic track record of live performance.

Regular backtests overfit the entire dataset. Walk forward testing algos use only unseen OOS data for validation across dozens of periods, delivering honest, regime-adaptive results that survive 2026 volatility.

QuantConnect (native scheduling), MetaTrader 5 (built-in), TradingView (custom Pine scripts), and Python/Blueshift. All work seamlessly for US futures.

Absolutely. Optimize in TradingView, then automate live on Tradovate/Rithmic via PickMyTrade across multiple funded accounts—perfect for ES, NQ, and other contracts.

Disclaimer:

This content is for informational purposes only and does not constitute financial, investment, or trading advice. Trading and investing in financial markets involve risk, and it is possible to lose some or all of your capital. Always perform your own research and consult with a licensed financial advisor before making any trading decisions. The mention of any proprietary trading firms, brokers, does not constitute an endorsement or partnership. Ensure you understand all terms, conditions, and compliance requirements of the firms and platforms you use.

Also Checkout: Event-Based Trading: Triggers vs Time-Based Strategies